BDMS– คงเป้าหมายปี 2567 เน้นขยายเครือข่ายในต่างจังหวัด – OUTPERFORM (ราคาเป้าหมาย 36 บาท)

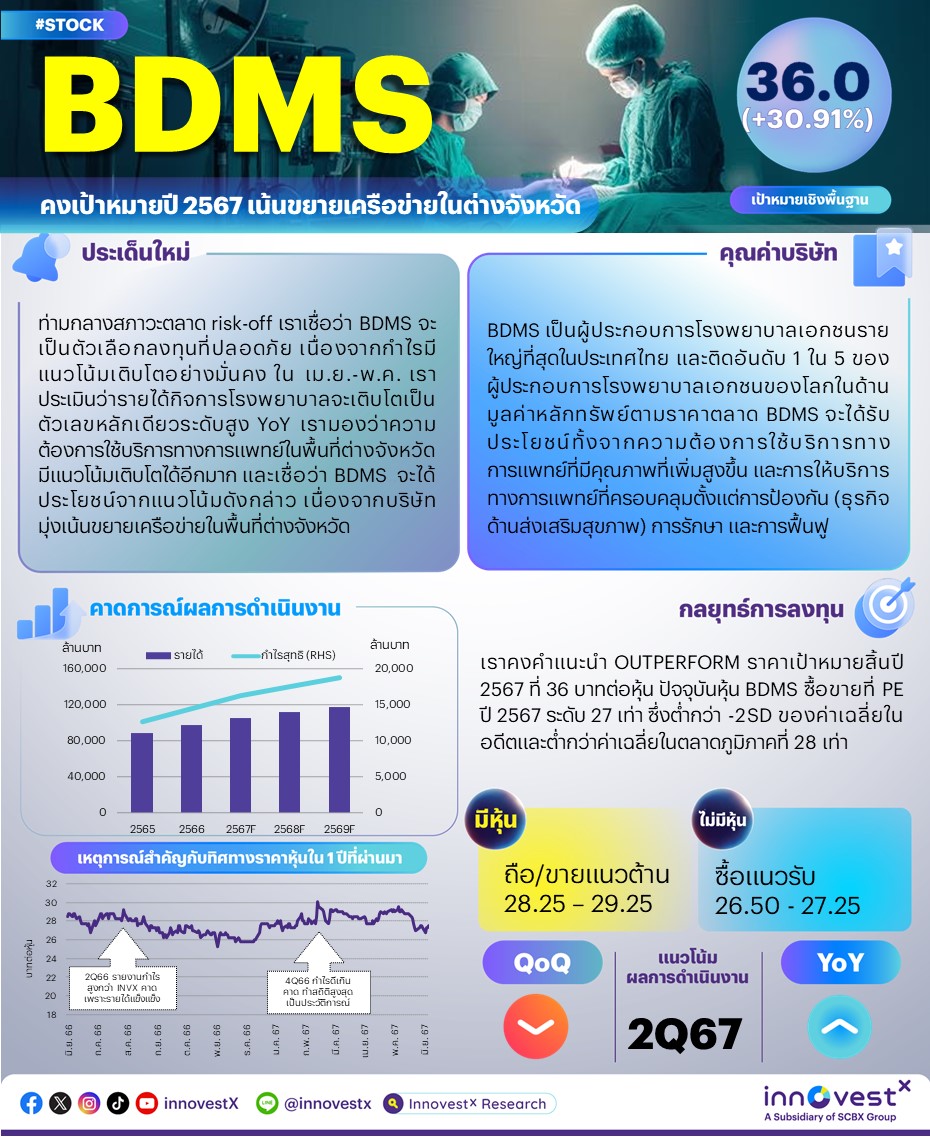

ท่ามกลางสภาวะตลาด risk-off เราเชื่อว่า BDMS จะเป็นตัวเลือกลงทุนที่ปลอดภัย เนื่องจากกำไรมีแนวโน้มเติบโตอย่างมั่นคง ในเดือนเม.ย.-พ.ค. เราประเมินว่ารายได้กิจการโรงพยาบาลของ BDMS จะเติบโตเป็นตัวเลขหลักเดียวระดับสูง YoY (ต่อเนื่องจากที่เติบโต 11% YoY ใน 1Q67) เรามองว่าความต้องการใช้บริการทางการแพทย์ในพื้นที่ต่างจังหวัดมีแนวโน้มเติบโตได้อีกมาก และเชื่อว่า BDMS จะได้ประโยชน์จากแนวโน้มดังกล่าว เนื่องจากบริษัทมุ่งเน้นขยายเครือข่ายโรงพยาบาลในพื้นที่ต่างจังหวัด ปัจจุบันหุ้น BDMS ซื้อขายที่ PE ปี 2567 ระดับ 27 เท่า ซึ่งต่ำกว่าระดับ -2SD ของค่าเฉลี่ยในอดีต และต่ำกว่าค่าเฉลี่ยในตลาดภูมิภาคที่ 28 เท่า เรายังคงคำแนะนำ tactical call ระยะ 3 เดือน สำหรับ BDMS ไว้ที่ OUTPERFORM โดยให้ราคาเป้าหมายสิ้นปี 2567 อ้างอิงวิธี DCF ที่ 36 บาท/หุ้น BDMS เป็นหนึ่งในหุ้นเด่นของเราในกลุ่มการแพทย์

BDMS คงเป้าหมายปี 2567 BDMS ยังคงเป้าการเติบโตของรายได้ไว้ที่ 10-12% และ EBITDA margin ที่ 24-25% ในปี 2567 โดยในเดือนเม.ย.-พ.ค. เราประเมินว่ารายได้กิจการโรงพยาบาลของ BDMS จะเติบโตเป็นตัวเลขหลักเดียวระดับสูง YoY (ต่อเนื่องจากที่เติบโต 11% YoY ใน 1Q67) โดยได้แรงหนุนหลักจากการกลับมาของผู้ป่วยชาวไทยหลังจากหยุดเทศกาลสงกรานต์ในเดือนเม.ย. กลุ่มผู้ป่วยประกันสุขภาพภาคเอกชนที่เพิ่มขึ้น ซึ่งคิดเป็น 38% ของรายได้ใน 1Q67 (เพิ่มขึ้นจาก 36% ในปี 2566) และจำนวนผู้ป่วยชาวต่างชาติที่เพิ่มขึ้น ผู้ป่วยชาวคูเวต (ที่ค่ารักษาพยาบาลได้รับเงินสนับสนุนจากรัฐบาลคูเวต) ยังมีแนวโน้มลดลงต่อเนื่องใน 2Q67 เนื่องจากรัฐบาลคูเวตยังคงอยู่ในกระบวนการรวบรวมรายชื่อโรงพยาบาลไทยที่มีคุณสมบัติและสามารถเบิกจ่ายได้ ส่งผลทำให้มีการชะลอการเดินทางเข้ามารับการรักษาพยาบาล เราคาดว่าผลกระทบต่อ BDMS จะมีจำกัด เนื่องจาก BDMS มีรายได้จากการให้บริการผู้ป่วยชาวต่างชาติมีการกระจายตัว และรายได้จากผู้ป่วยชาวคูเวตคิดเป็นสัดส่วนไม่ถึง 1% ของรายได้รวม

เน้นขยายเครือข่ายในพื้นที่ต่างจังหวัด เรามองว่าความต้องการใช้บริการทางการแพทย์ในพื้นที่ต่างจังหวัดมีแนวโน้มเติบโตได้อีกมากด้วยแรงหนุนจากอุตสาหกรรมท่องเที่ยวที่กำลังเติบโตและภาพรวมอุตสาหกรรมที่เป็นบวกเพราะแนวโน้มความต้องการรักษาพยาบาลเพิ่มขึ้น ในขณะที่อุปทานมีน้อย โดยในปี 2565 ประเทศไทยมีจำนวนเตียงผู้ป่วย 2.6 เตียงต่อประชากร 1,000 คน โดยแบ่งเป็น 5.5 เตียงในกรุงเทพฯ และ 2.1-2.7 เตียงในภูมิภาคอื่นๆ ใน 1Q67 รายได้จากโรงพยาบาลในพื้นที่ต่างจังหวัดของ BDMS เติบโต 16% YoY ซึ่งมากกว่ารายได้จากโรงพยาบาลในพื้นที่กรุงเทพฯ และปริมณฑลที่เติบโต 7% YoY และคิดเป็น 46% ของรายได้กิจการโรงพยาบาลรวมทั้งหมด (เพิ่มขึ้นจาก 42% ในปี 2562 และ 44% ในปี 2566) เราเชื่อว่าแนวโน้มที่แข็งแกร่งนี้จะดำเนินต่อไป เนื่องจาก BDMS จะเน้นขยายเครือข่ายโรงพยาบาลในพื้นที่ต่างจังหวัด โดยบริษัทวางแผนเพิ่มจำนวนเตียงเป็น ~9,300 เตียงในปี 2569-2570 (จาก ~8,600 เตียงในปี 2566) และ 65% ของจำนวนเตียงที่เพิ่มขึ้นอยู่ในพื้นที่ต่างจังหวัด BDMS ได้เปิดโรงพยาบาลใหม่ พญาไท ศรีราชา 2 ที่จังหวัดชลบุรี ในเดือนมี.ค. และศูนย์สุขภาพ BDMS Wellness Clinic สองแห่งที่ภูเก็ตในเดือนมิ.ย. นอกจากนี้ BDMS ยังวางแผนที่จะเปิดศูนย์มะเร็งที่โรงพยาบาลสิริโรจน์ ซึ่งจะเป็นศูนย์รังสีรักษาแห่งแรกในภูเก็ตใน 3Q67 ด้วย

ประมาณการของเราบ่งชี้ว่ากำไรจะแข็งแกร่งขึ้นใน 2H67 เราคาดว่ากำไรปกติจะเติบโต YoY ต่อเนื่องใน 2Q67 แต่จะลดลง QoQ จากปัจจัยฤดูกาล เรายังคงคาดการณ์ว่ากำไรปกติปี 2567 จะเติบโต 13% YoY สู่ 1.6 พันลบ. ซึ่งบ่งชี้ว่าการดำเนินงานและกำไรจะแข็งแกร่งขึ้นใน 2H67 ราคาเป้าหมายสิ้นปี 2567 อ้างอิงวิธี DCF ของเราอยู่ที่ 36 บาท/หุ้น (WACC ที่ 7.1% และการเติบโตระยะยาวที่ 3%)

ความเสี่ยง เรากำลังจับตาดูการชะลอตัวของเศรษฐกิจโลกและความเสี่ยงด้านภูมิรัฐศาสตร์ที่อาจทำให้เกิดการชะลอการรักษาโรคที่ไม่เร่งด่วนและความไม่สะดวกของผู้ป่วยต่างชาติที่จะเดินทางมารับการรักษาพยาบาลในประเทศไทย อย่างไรก็ดี เรามองว่าความเสี่ยงนี้น่าจะลดทอนลงได้ เนื่องจาก BDMS มีฐานรายได้ขนาดใหญ่จากผู้ป่วยชาวไทย ในขณะที่รายได้จากการให้บริการผู้ป่วยชาวต่างชาติมีการกระจายตัว เรามองว่าปัจจัยเสี่ยงด้าน ESG คือ ความปลอดภัยของผู้ป่วย (S) ซึ่ง BDMS ได้นำเอาระบบบริหารคุณภาพต่างๆ มาใช้สำหรับกระบวนการดูแลผู้ป่วยอย่างต่อเนื่อง

ท่านสามารถอ่านและดาวน์โหลดเอกสารได้จาก BDMS240614_T

Amid this risk-off market, we see BDMS as a safe investment in view of its resilient and steady earnings uptrend. In April-May, we estimate hospital revenue growth in the high single digits YoY, continuing from 11% YoY in 1Q24. We see more potential for growth in health demand upcountry and believe BDMS will capture this as it focuses on expanding upcountry. BDMS is trading at 27x 2024PE, below -2SD of its historical average and below the regional average of 28x. We maintain our 3-month tactical call of Outperform with end-2024 DCF TP of Bt36/share. BDMS is one of our top picks in the Healthcare Service sector.

BDMS stands by its 2024 targets. BDMS is maintaining its targets of 10-12% revenue growth with a 24-25% EBITDA margin in 2024. By our estimates, in April-May hospital revenue grew in the high single digits YoY, continuing from 11% YoY growth in 1Q24, backed by the return of Thai patients after the long Songkran holiday in April, a growing private insurance segment (up to 38% of 1Q24 revenue from 36% in 2023) and more international patients. The number of Kuwaiti patients (whose healthcare is covered by the government) continued to decline in 2Q24 as they wait for their government to complete a list of qualifying Thai hospitals. We see the delay as having limited impact on BDMS given its diversified portfolio of international patient services and the fact that revenue from Kuwaiti patients comprises than 1% of its revenue.

Expansion to focus on provinces. We see more potential for health demand growth upcountry, driven by growing Thai tourism and an environment where demand is rising while supply is low: in 2022, Thailand had 2.6 beds per 1,000 population, consisting of 5.5 in Bangkok and 2.1-2.7 for other regions. In 1Q24, BDMS’ revenue from hospitals outside Bangkok grew 16% YoY, beating metropolitan Bangkok’s 7% YoY, to take 46% of total hospital revenue (up from 42% in 2019 and 44% in 2023). We expect this strong uptrend will continue as BDMS focuses on expansion upcountry: it plans to increase bed capacity to ~9,300 beds in 2026-27 (from ~8,600 in 2023), with 65% of those upcountry. BDMS opened a new hospital, Phyathai Sriracha 2, in Chonburi in March and two BDMS Wellness Clinic centers in Phuket in June. It plans to open a cancer center at Siriroj Hospital which will be Phuket’s first radiology center, in 3Q24.

Our forecast suggests stronger 2H24. We expect core earnings to continue to grow YoY in 2Q24 but drop QoQ on seasonality. We maintain our forecast of 2024 core earnings growth of 13% YoY to Bt16bn, suggesting stronger operations and earnings in 2H24. Our end-2024 DCF TP is Bt36/share (WACC at 7.1% and LT growth at 3%).

Risks. We are keeping an eye on the global economic slowdown and geopolitical risk that may cause clients to delay elective medical care and make it inconvenient for international patients to come to Thailand for treatment. However, we see this risk as diluted by BDMS’ large revenue base from Thai patients and its diversified portfolio of international patient services. We see ESG risk as patient safety (S): BDMS has adopted a variety of quality assurance systems to provide continuous patient care.

Click here to read and/or download BDMS240614_E