เราปรับคำแนะนำสำหรับ BAM ขึ้นเป็น OUTPERFORM โดยคงราคาเป้าหมายไว้ที่ 8 บาท เนื่องจากราคาหุ้นปรับตัวลดลงมาแล้ว 20% หลังจากประกาศผลประกอบการ 2Q68 และอัตราผลตอบแทนจากเงินปันผลดีที่ 7.35% เมื่อพิจารณาจากผลเรียกเก็บที่เพิ่มขึ้นอย่างมีนัยสำคัญ กำไรที่คาดว่าจะเติบโตอย่างแข็งแกร่ง และการซื้อ NPL น้อยลง เราคาดว่า BAM จะเพิ่ม DPS จาก 0.35 บาท ในปี 2567 เป็น 0.5 บาท (อัตราการจ่ายเงินปันผล 72%) ในปี 2568 เราคาดว่ากำไรสุทธิ 3Q68 จะอยู่ในระดับทรงตัว YoY แต่จะลดลงมาก QoQ เพราะกำไรจะกลับคืนสู่ระดับปกติหลังจากออกมาดีมากเป็นพิเศษใน 2Q68 กำไรสุทธิจะกลับมาเพิ่มขึ้น QoQ ใน 4Q68 จากผลเรียกเก็บที่เพิ่มขึ้นตามฤดูกาล

คาดกำไรสุทธิทรงตัว YoY แต่ลดลง QoQ ใน 3Q68 ก่อนจะปรับตัวเพิ่มขึ้นใน 4Q68 เราคาดว่ากำไรสุทธิ 3Q68 ของ BAM จะอยู่ที่ 203 ลบ. (+2% YoY, -84% QoQ) โดยอิงกับการคาดการณ์ว่าผลเรียกเก็บจะเพิ่มขึ้น 5% YoY แต่ลดลง 48% QoQ มาอยู่ที่ 3.6 พันลบ. เราคาดว่า ECL ใน 3Q68 จะมากกว่ารายได้ดอกเบี้ยค้างรับ ซึ่งเป็นผลมาจากการตั้งสำรองเพิ่มเติมสำหรับต้นทุนส่วนที่เหลือของสินทรัพย์รอการขาย (NPA) ที่ได้จากกรมบังคับคดี อย่างไรก็ตาม เราคาดว่ากำไรสุทธิจะกลับมาปรับตัวเพิ่มขึ้น QoQ ใน 4Q68 จากผลเรียกเก็บที่เพิ่มขึ้นตามฤดูกาล

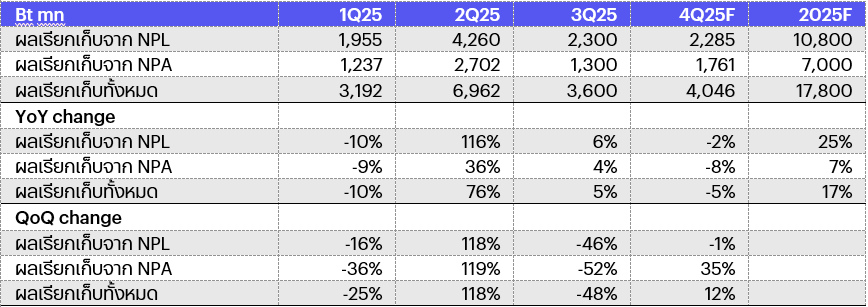

คาดผลเรียกเก็บในปี 2568 เพิ่มขึ้นมากตามเป้า เราคาดว่า BAM จะเพิ่มผลเรียกเก็บได้ตามเป้าที่บริษัทวางไว้ที่ 17% เป็น 1.78 หมื่นลบ. ในปี 2568 ซึ่งเป็นระดับสูงที่สุดนับตั้งแต่ปี 2563 โดยหลังจากมีผลเรียกเก็บสูงมากเป็นพิเศษที่ 6.96 พันลบ. (+76% YoY, +118% QoQ) ซึ่งหลักๆ เกิดจาก NPA (1.45 พันลบ.) และ NPL (2.8 พันลบ.) รายใหญ่ใน 2Q68 ผลเรียกเก็บของ BAM ก็กลับมาอยู่ที่ระดับปกติที่ราว 3.6 พันลบ. (+5% YoY, -48% QoQ) ใน 3Q68 เราคาดว่าผลเรียกเก็บจะเพิ่มขึ้น 12% QoQ ตามฤดูกาล (-5% YoY) มาอยู่ที่ราว 4 พันลบ. ใน 4Q68 โดยส่วนหนึ่งมาจาก NPL และ NPA รายใหญ่ (อย่างละ 50 ลบ.)

Figure 1: ผลเรียกเก็บของ BAM

Source: BAM and InnovestX Research

ซื้อ NPL น้อยลง BAM ได้เข้าซื้อ NPL มูลค่าราว 900 ลบ. (มูลค่าสิทธิเรียกร้อง 3 พันลบ.) ใน 9M68 ต่ำกว่าเป้าที่บริษัทวางไว้ทั้งปีที่ 8 พันลบ. ค่อนข้างมาก เนื่องจากธนาคารต่างๆ ชะลอการขาย NPL เพราะราคาไม่เป็นที่น่าพอใจ เราคาดว่า BAM จะซื้อ NPL 3 พันลบ. ในปี 2568

อัตราผลตอบแทนจากเงินปันผลดี เมื่อพิจารณาจากผลเรียกเก็บที่คาดว่าจะเพิ่มขึ้น 17% กำไรที่คาดว่าเติบโต 39% และการซื้อ NPL น้อยลง เราคาดว่า BAM จะเพิ่ม DPS จาก 0.35 บาท ในปี 2567 เป็น 0.5 บาท (อัตราการจ่ายเงินปันผล 72%) ในปี 2568 คิดเป็นอัตราผลตอบแทนจากเงินปันผล 7.35%

ปรับคำแนะนำขึ้นเป็น OUTPERFORM โดยคงราคาเป้าหมายไว้เช่นเดิม เราปรับคำแนะนำสำหรับ BAM ขึ้นเป็น OUTPERFORM โดยคงราคาเป้าหมายไว้ที่ 8 บาท (อิงกับวิธี DDM) เนื่องจากราคาหุ้นปรับตัวลดลงมาแล้ว 20% หลังจากประกาศผลประกอบการ 2Q68 ทำให้เราคาดการณ์ถึงอัตราผลตอบแทนจากเงินปันผลที่ดีที่ 7.35%

ปัจจัยเสี่ยงที่สำคัญ: 1) ความเสี่ยงด้านการเรียกเก็บเงินสดจากภาวะเศรษฐกิจชะลอตัว 2) อุปสงค์ในตลาดอสังหาริมทรัพย์ชะลอตัวลง และ 3) การแข่งขันที่สูงขึ้นจากผู้เล่นรายใหม่

We expect 2Q25 earnings to surge 174% YoY and 477% QoQ on exceptionally high cash collection from a large NPA and an NPL. We raise our 2025F by 19% and now expect growth of 40% in 2025F. Dividend yield in 2025 is expected to be decent at 6%. We maintain Neutral with a lift in TP to Bt8 from Bt7. We believe the exceptionally good 2Q25 results have been priced in and is unsustainable.

Preview 3Q25F: Weak; upgrade as dividend play

We upgrade BAM to Outperform with an unchanged TP of Bt8 in response to a 20% fall in share price after 2Q25 results and a good dividend yield of 7.35%. As a result of a substantial rise in cash collection, strong earnings growth and lower NPL purchases, we expect BAM to raise DPS to Bt0.5 (72% payout) on 2025 from Bt0.35 on 2024. We expect 3Q25F earnings to be flattish YoY but down sharply QoQ on a return to normal from the exceptionally good 2Q25. We expect 4Q25F earnings to rise QoQ in 4Q25 from a seasonal rise in cash collection.

Expect earnings to be flat YoY and down QoQ in 3Q25 before up in 4Q25. We forecast 3Q25F earnings of Bt203mn (+2% YoY, -84% QoQ), based on expectation of a 5% YoY rise but a 48% QoQ fall in cash collection to Bt3.6bn. We expect 3Q25F ECL to be larger than accrued interest income due to addition of reserve for the remaining cost of NPAs obtained from the Legal Execution Department. We expect 4Q25F earnings to swing up QoQ in 4Q25 from a seasonal rise in cash collection.

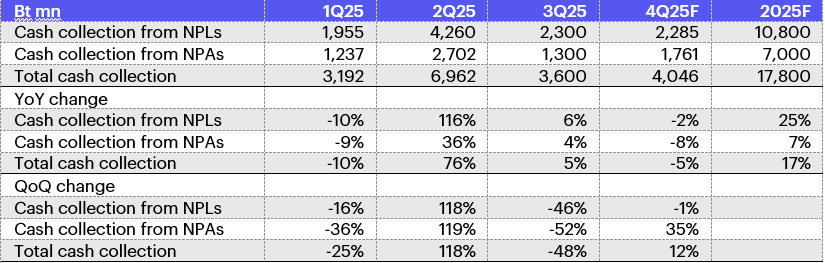

Expect a good rise in 2025F cash collection as targeted. We expect BAM to achieve its target to boost cash collection by 17% to Bt17.8bn in 2025, the highest since 2020. After the exceptionally high cash collection in 2Q25 of Bt6.96bn (+76% YoY, +118% QoQ) mainly from large NPAs (Bt1.45bn) and NPLs (Bt2.8bn), cash collection returned to a normal level of ~Bt3.6bn (+5% YoY, -48% QoQ) in 3Q25. We expect cash collection to rise 12% QoQ (-5% YoY) on seasonality to ~Bt4bn in 4Q25 on collections from large NPLs and NPAs (Bt50mn each).

Figure 1: BAM’s cash collection

Source: BAM and InnovestX Research

Falling NPL purchases. BAM invested ~Bt900mn (Bt3bn claim value) in NPLs in 9M25, well behind its full-year target of Bt8bn, as banks put off NPL sales due to unsatisfactory pricing. We expect NPL purchases to be Bt3bn in 2025.

Good dividend yield. Due to an expectation of a 17% rise in cash collection, a 39% earnings growth and smaller NPL purchases, we expect BAM to increase DPS from Bt0.35 on 2024 to Bt0.5 (72% payout) on 2025, equivalent to 7.35% yield.

Upgrade to Outperform with an unchanged TP. We upgrade BAM to Outperform with an unchanged TP of Bt8 (based on DDM) due to a 20% fall in share price post 2Q25 results, which translates to expectation of good dividend yield of 7.35%.

Key risks: 1) Cash collection risk from an economic slowdown, 2) a slowdown in property market demand and 3) rising competition from new players.

Download PDF Click > BAM251031_E.pdf