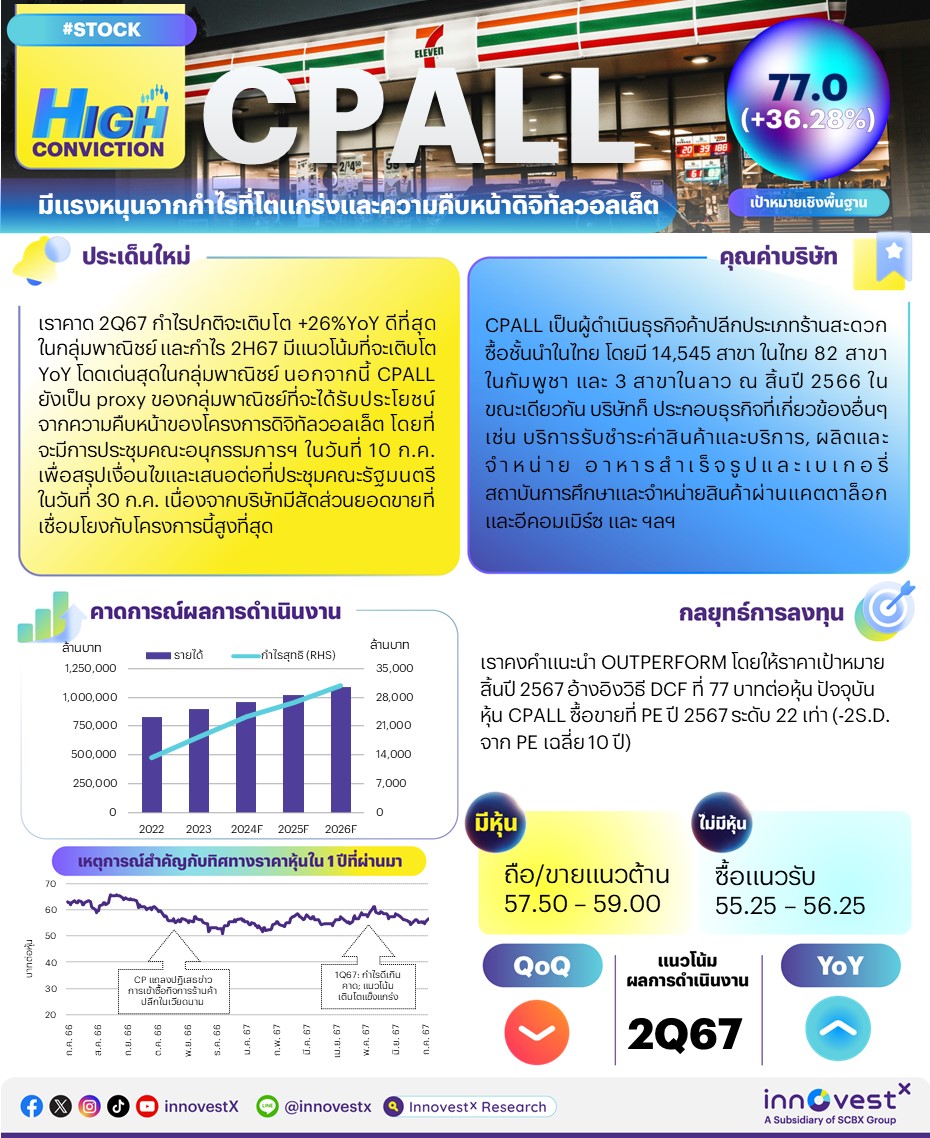

High Conviction: CPALL มีแรงหนุนจากกําไรที่โตแกร่งและความคืบหน้าดิจิทัลวอลเล็ต – OUTPERFORM (ราคาเป้าหมาย 77 บาท)

เราคาดว่า CPALL จะรายงานกําไรปกติ 2Q67 เติบโต YoY ดีที่สุดในกลุ่มพาณิชย์ที่ +26% YoY โดยได้รับ การสนับสนุนจากยอดขายและมาร์จิ้นที่ดีขึ้น และส่วนแบ่งกําไรที่เพิ่มขึ้นจาก CPAXT กําไร 2H67 ของ CPALL มีแนวโน้มที่จะเติบโต YoY โดดเด่นมากกว่าบริษัทอื่นๆ ในกลุ่มพาณิชย์ โดยเกิดจากการเติบโตที่ แข็งแกร่งทั้งจากธุรกิจ CVS และ CPAXT นอกจากนี้ CPALL ยังเป็น proxy ของกลุ่มพาณิชย์ที่จะได้รับ ประโยชน์จากความคืบหน้าของโครงการดิจิทัลวอลเล็ต (เพิ่ม upside หากเริ่ มใช้ใน 4Q67 ซึ่งยังไม่ รวฃมอยู่ในประมาณการของเรา) โดยที่จะมีการประชุมคณะอนุกรรมการฯ ในวันที่ 10 ก.ค. เพื่อสรุปเงื่อนไข และเสนอต่อที่ประชุมคณะรัฐมนตรีในวันที่ 30 ก.ค. เนื่องจากบริษัทมีสัดส่วนยอดขายที่เชื่อมโยงกับ โครงการนี้สูงที่สุด ปัจจุบันหุ้น CPALL ซื้อขายที่ PE ปี 2567 ระดับ 22 เท่า (-2S.D. จาก PE เฉลี่ย 10 ปี) จากประเด็นทั้งหมดที่กล่าวมา ทําให้เราคาดว่าราคาหุ้น CPALL ซึ่งยังคง underperformance 3% เทียบ กับ SET ใน 1 เดือนที่ผ่านมา น่าจะปรับตัวดีขึ้น เรายังคงคําแนะนํา OUTPERFORM สําหรับ CPALL โดยให้ ราคาเป้าหมายสิ้นปี 2567 อ้างอิงวิธี DCF (WACC 7%, การเติบโตระยะยาว 2.5%) ที่ 77 บาท

ปัจจัยกระตุ้น#1: กําไร 2Q67 จะเติบโต YoY ดีที่สุดในกลุ่มพาณิชย์ เราคาดว่า CPALL จะรายงานกําไร สุทธิ 2Q67 ที่ 5.8 พันลบ. +31% YoY แต่ -8% QoQ หากตัดรายการพิเศษ (-162 ลบ. ใน 2Q66 และ +298 ลบ. ใน 1Q67) ออกไป กําไรปกติ 2Q67 จะอยู่ที่ 5.8 พันลบ. +26% YoY แต่ -4% QoQ โดยกําไรปกติจะเติบโต YoY ดีที่สุดในกลุ่มพาณิชย์ด้วยแรงหนุนจากปัจจัยดังต่อไปนี้ ปัจจัยแรก ยอดขายจากธุรกิจ CVS จะปรับตัวเพิ่มขึ้นผ่านการเติบโตของ SSS ที่ +4% YoY (เทียบกับ +4.9% YoY ใน 1Q67) และการขยายสาขา (+150 สาขา สู่ 14,880 สาขา, +5% YoY และ +1% QoQ) ปัจจัยที่สอง อัตรากําไรขั้นต้นจากธุรกิจ CVS จะ กว้างขึ้น YoY จากยอดขายสินค้ากลุ่มของใช้ส่วนตัวและ ready-to-eat (RTE) ที่มีมาร์จิ้นสูงที่เพิ่มขึ้นสืบเนื่องมาจากการกลับมาของนักท่องเที่ยวและการซื้อแบบไม่ได้วางแผนไว้ล่วงหน้าเพิ่มมากขึ้น และการ ลดลงของยอดขายบุหรี่ที่มีมาร์จิ้นตํ่า ปัจจัยที่สาม อัตราส่วนค่าใช้จ่าย SG&A/ยอดขายจะอยู่ภายใต้การ ควบคุมซึ่งเป็นผลมาจากต้นทุนค่าไฟฟ้าที่ลดลง และการควบคุมต้นทุนอื่นๆ ท่ามกลางยอดขายที่เพิ่มขึ้น ปัจจัยสุดท้าย ส่วนแบ่งกําไรจาก CPAXT จะเพิ่ มข้ึน โดยที่เราประเมินกําไรปกติ 2Q67 ได้ที่ 2 พันลบ. +20% YoY จากยอดขายและ EBIT margin ที่ดีขึ้น (อัตรากําไรขั้นต้นกว้างขึ้นและอัตราส่วนค่าใช้จ่าย SG&A/ ยอดขายลดลง) แต่ -18% QoQ จากปัจจัยฤดูกาล

ปัจจัยกระตุ้น#2: คาดกําไรเติบโตแข็งแกร่ง YoY ใน 2H67 เราคาดว่ากําไรปกติ 2H67 ของ CPALL จะ เติบโต YoY โดดเด่นมากกว่าบริษัทอื่นๆ ในกลุ่มพาณิชย์ โดยเกิดจากการเติบโตทั้งจากธุรกิจ CVS (ยอดขายและมาร์จิ้นเพิ่มขึ้นจากการกลับมาของนักท่องเที่ยว การซื้อแบบไม่ได้วางแผนไว้ล่วงหน้าเพิ่มมากขึ้น ประกอบการนําเสนอสินค้าใหม่ที่มีมาร์จิ้นสูง เช่น สินค้ากลุ่ม RTE และ RTD) และ CPAXT (ยอดขายและ มารจิ้ นปรับตัวดีขึ้น ซึ่งเกิดจากทั้งธุรกิจ B2B และธุรกิจ B2C)

ปัจจัยกระตุ้น#3: Proxy ของกลุ่มพาณิชย์ที่จะได้รับประโยชน์จากโครงการดิจิทัลวอลเล็ต เมื่อวันที่ 8 ก.ค. รัฐมนตรีช่วยว่าการกระทรวงการคลังของไทยยืนยันว่าโครงการดิจิทัลวอลเล็ตยังคงอยู่ในไทม์ไลน์ โดยจะมีการประชุมคณะอนุกรรมการฯ ในวันที่ 10 ก.ค. เพื่อสรุปเงื่อนไข ตามด้วยการประชุม คณะกรรมการนโยบายซึ่งมีนายกรัฐมนตรีเป็นประธานในวันที่ 15 ก.ค. จากนั้นนายกรัฐมนตรีจะแถลง รายละเอียดโครงการในวันที่ 24 ก.ค. ก่อนจะนําเข้าสู่ที่ประชุมคณะรัฐมนตรีในวันที่ 30 ก.ค. การนําเรื่อง ปรึกษากับคณะกรรมการกฤษฎีกาจะเกิดขึ้นหลังจากวันที่ 30 ก.ค. ทั้งนี้เรายังไม่ได้รวม upside ของกําไรที่ อาจเกิดขึ้นจากโครงการดิจิทัลวอลเล็ตเข้ามา หากโครงการนี้ดําเนินการได้ใน 4Q67 เราประเมินได้ว่า CPALL จะเป็นผู้ที่ได้รับประโยชน์มากที่สุดในกลุ่มพาณิชย์ เนื่องจากยอดขาย 56% ในงบการเงินรวมของ CPALL เชื่อมโยงกับโครงการนี้ผ่านทางร้านสะดวกซื้อของบริษัทและยอดขายจาก CPAXT ที่มาจากร้านค้าปลีกรายย่อยและร้านค้าส่งในธุรกิจ B2B และร้านค้าขนาดเล็กในธุรกิจ B2C

ปัจจัยเสี่ยงที่สําคัญ คือ การเปลี่ยนแปลงในกําลังและนโยบายของรัฐบาล ความเสี่ยง ESG ที่สําคัญ คือ การบริหารจัดการพลังงาน ผลิตภัณฑ์ ที่ยั่งยืน (E) และแนวปฏิบัติด้านการจางงาน (S)

ท่านสามารถอ่านและดาวน์โหลดเอกสารได้จาก CPALL_HighConviction240709_T

|