High Conviction: CPALL – คาดกำไร 1Q67 เติบโต YoY ดีที่สุดในกลุ่มพาณิชย์ – OUTPERFORM (ราคาเป้าหมาย 75 บาท)

|

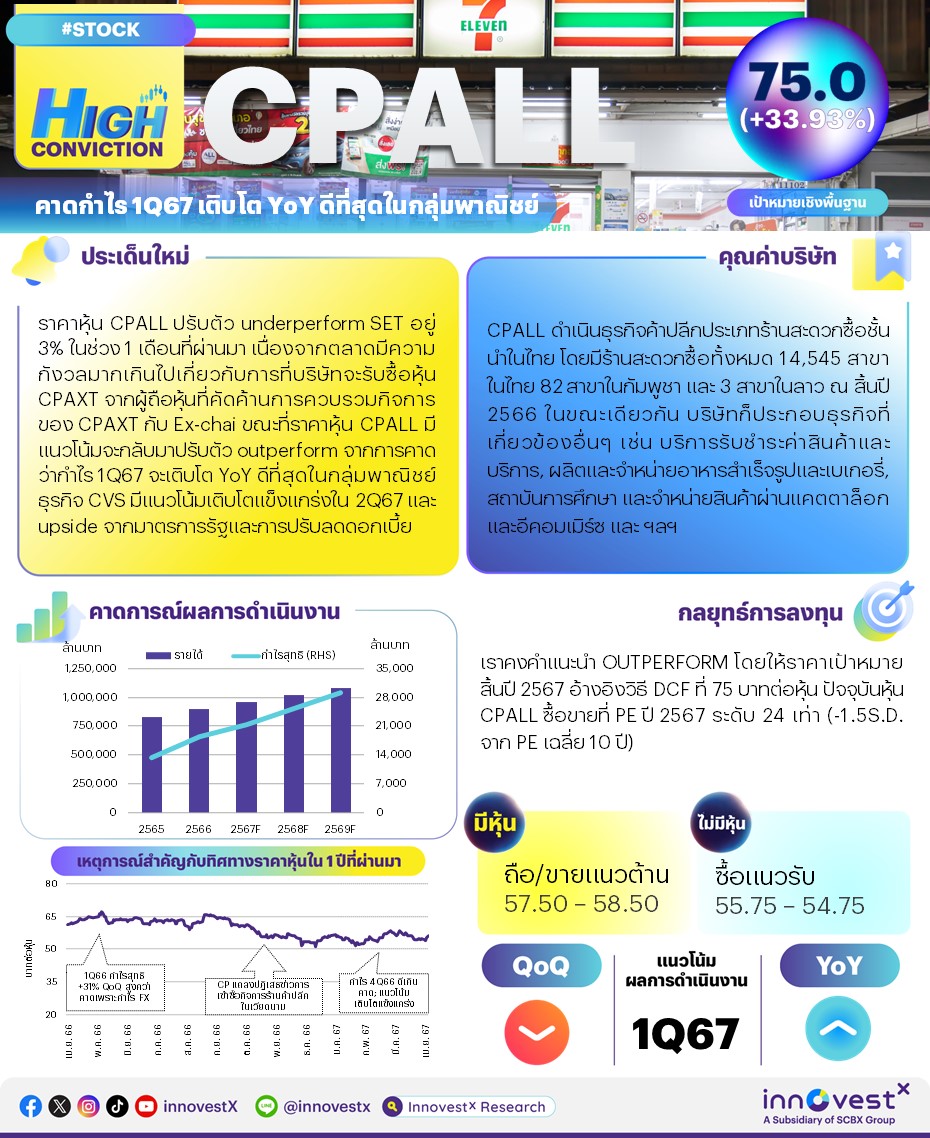

ราคาหุ้น CPALL ปรับตัว underperform SET อยู่ 3% ในช่วง 1 เดือนที่ผ่านมา เนื่องจากตลาดมีความกังวลมากเกินไปเกี่ยวกับการที่บริษัทจะรับซื้อหุ้น CPAXT จากผู้ถือหุ้นที่คัดค้านการควบรวมกิจการของ CPAXT กับ Ex-chai (CPALL จะใช้เงินเพียง 14 ลบ. สำหรับธุรกรรมนี้ โดยอิงกับมติที่ประชุมสามัญผู้ถือหุ้นของ CPAXT เมื่อวันที่ 29 มี.ค.) ราคาหุ้น CPALL มีแนวโน้มจะกลับมาปรับตัว outperform จากการคาดการณ์ว่ากำไร 1Q67 จะเติบโต YoY ดีที่สุดในกลุ่มพาณิชย์ SSS ของธุรกิจ CVS มีแนวโน้มเติบโตแข็งแกร่งใน 2Q67 จากนักท่องเที่ยวที่เพิ่มขึ้นและอากาศร้อน และ upside จากมาตรการ digital wallet และการปรับลดอัตราดอกเบี้ยนโยบาย ปัจจุบันหุ้น CPALL ซื้อขายที่ PE ปี 2567 ระดับ 24 เท่า (-1.5S.D. จาก PE เฉลี่ย 10 ปี) คงคำแนะนำ OUTPERFORM โดยมีราคาเป้าหมายสิ้นปี 2567 วิธี DCF ที่ 75 บาท

|

|---|

ท่านสามารถอ่านและดาวน์โหลดเอกสารได้จาก CPALL_HighConviction240409_T

CPALL share price has underperformed the SET by 3% over the past month as market concern on its purchase of shares from CPAXT dissenting shareholders in the amalgamation of CPAXT and Ex-Chai is overdone. Based on the Mar 29 AGM resolution, CPALL will spend only Bt14mn on this transaction. Price is expected to turn up to outperform as it is poised to report the sector’s best 1Q24F growth YoY, its upcoming strong CVS SSS growth in 2Q24F from more tourists and hot weather, plus upside from the Digital Wallet and a cut in policy rate. CPALL is now trading at 24x 24PE (-1.5S.D. over its 10-year PE). Maintain Outperform with an end-2024 DCF TP of Bt75.

Catalyst #1: 1Q24F to top the sector YoY. We expect CPALL to report a 1Q24F net profit of Bt5bn, +22% YoY but -8% QoQ. Removing extra items (+Bt344mn in 1Q23 and -Bt116mn in 4Q23) uncovers 1Q24F core profit of Bt5bn, +34% YoY but

-10% QoQ. Several factors underwrite the YoY jump. First, CVS sales will be raised via SSS growth of +4% YoY (vs +3.6% YoY in 4Q23) and store expansion (+150 stores to 14,695 stores, +5% YoY and +1% QoQ), with a wider gross margin at CPRAM from lower swine raw material costs and more sales of high-margin personal care and ready-to-eat (RTE) items brought by the return of tourists and more impulse buying, and lower SG&A/sales from lower electricity costs. Second, we expect better contribution from CPAXT with 1Q24F core profit of Bt2.5bn, +21% YoY from better sales and EBIT margin, and lower interest expenses from debt refinancing but -23% QoQ from seasonality. It will release results on May 10.

Catalyst #2: Other catalysts lined up. First, SSS should continue to grow strongly YoY in 2Q24F, boosted by more international tourists, particularly the visa-free entry granted Chinese from March, and more local tourists during the long holiday plus hotter weather. TMD forecasts temperatures to hover at 1-1.5 degrees Celsius above average in 2Q24F, which will lift RTE and RTD sales. Second, based on news about the digital wallet, CPALL is positioned to gain the most in its sector, as it is the only company that has 100% store coverage of all districts in Thailand. If approved, there will be sales and earnings upside in 4Q24F. Third, INVX expects the BoT to cut interest rate by 50bps YoY in 2024, starting in 2Q24. This will add 4% to its earnings, based on its floating rate and the current portion of fixed-rate interest-bearing debt.

Action & recommendation. CPALL has underperformed the SET by 3% over a month on overdone concerns about its purchase of shares from CPAXT dissenting shareholders in the amalgamation of CPAXT and Ex-Chai. Based on the resolution by CPAXT’s AGM on March 29, CPALL will use only Bt14mn (from internal cash flow) to purchase these shares. CPALL is ready to turn up to outperform as it is poised to report the sector’s best YoY growth in 1Q24F, with strong CVS SSS growth in 2Q24F and upside from the Digital Wallet and a cut in policy rate. Outperform with end-2024 DCF TP (WACC 7%, LT growth 2.5%) of Bt75.

Key risks are changes in purchasing power and government policies. Key ESG risks are energy management, sustainable products (E), and labor/employment practices (S).

Click here to read and/or download file CPALL_HighConviction240409_E