เราคาดว่ากำไรสุทธิ 1Q69 ของ BAM จะอยู่ในระดับทรงตัว YoY แต่เพิ่มขึ้น 84% QoQ โดยอิงกับผลเรียกเก็บที่ลดลง credit cost ที่ผ่อนคลายลง และต้นทุนทางการเงินที่ลดลง ทั้งนี้เพื่อสะท้อนแรงกดดันด้านเงินเฟ้อที่เพิ่มขึ้น เราจึงปรับประมาณการกำไรปี 2569 ลดลง 3% โดยปัจจุบันคาดว่ากำไรจะลดลง 5% เราคงคำแนะนำ OUTPERFORM สำหรับ BAM แต่ปรับราคาเป้าหมายลดลงจาก 8.5 บาท เป็น 7.5 บาท โดยมีปัจจัยหนุนจากอัตราตอบแทนเงินปันผลที่ดีที่ 6.6% และ upside จากโอกาสที่จะมีการจัดตั้ง JVAMC ใหม่

พรีวิว 1Q69: คาดกำไรทรงตัว YoY, เพิ่มขึ้น QoQ เราคาดว่ากำไรสุทธิ 1Q69 จะอยู่ในระดับทรงตัว YoY แต่เพิ่มขึ้น 84% QoQ มาอยู่ที่ 216 ลบ. โดยอิงกับ: 1) ผลเรียกเก็บที่ประเมินได้ที่ 3.0 พันลบ. ลดลง 6% YoY และ 26% QoQ 2) ECL ที่ลดลงจากการกันสำรองที่ลดลงสำหรับต้นทุนส่วนที่เหลือของ NPA ที่ซื้อมาจากกรมบังคับคดีและคุณภาพสินทรัพย์ที่แย่ลง 3) ต้นทุนทางการเงินที่ลดลงต่อเนื่อง 13 bps QoQ มาอยู่ที่ 3.27% และ 4) ค่าใช้จ่ายในการดำเนินงานที่ลดลงจากการรับรู้ผลขาดทุนจากการด้อยค่าของ NPA ที่น้อยลง

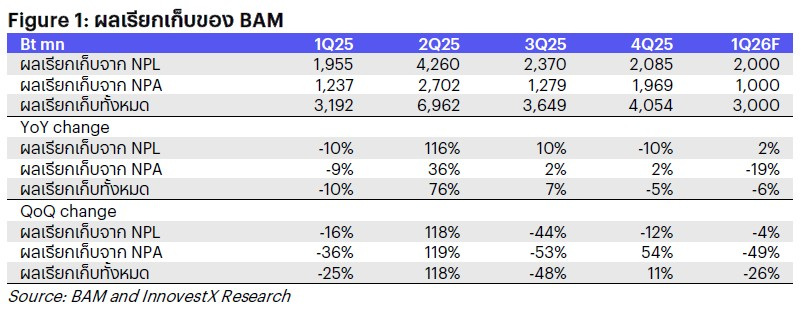

ผลเรียกเก็บ: ลดลง YoY และ QoQ; ปรับลดประมาณการปี 2569 จากการสอบถามเจ้าหน้าที่นักลงทุนสัมพันธ์ของ BAM พบว่าผลเรียกเก็บใน 1Q69 อยู่ที่ประมาณ 3 พันลบ. ลดลง 6% YoY และ 26% QoQ โดยตัวเลขผลเรียกเก็บที่ประเมินได้ใน 1Q69 ที่ 3.0 พันลบ. คิดเป็น 17% ของเป้าที่ BAM วางไว้ทั้งปีที่ 1.79 หมื่นลบ. แรงกดดันด้านเงินเฟ้อที่เพิ่มขึ้นจากวิกฤตพลังงานอันเนื่องมาจากความขัดแย้งในตะวันออกกลางส่งผลทำให้เราปรับสมมติฐานผลเรียกเก็บในปี 2569 ลดลงจาก 1.75 หมื่นลบ. เป็น 1.65 หมื่นลบ. ซึ่งคิดเป็นการลดลง 8% จากปี 2568 ที่มีฐานสูงจากดีล NPL และ NPA ขนาดใหญ่สองรายการ

ปรับลดประมาณการกำไรปี 2569 เราปรับประมาณการกำไรปี 2569 ลดลง 3% เนื่องจากเราปรับสมมติฐานผลเรียกเก็บลดลง 6% โดยปัจจุบันเราคาดว่ากำไรปี 2569 จะลดลง 5% โดยอิงกับผลเรียกเก็บที่คาดว่าจะลดลง 8% ต้นทุนทางการเงินที่ลดลง 20 bps credit cost ที่ลดลง 17 bps (จากกันสำรองที่ลดลงสำหรับ NPA ที่ซื้อมาจากกรมบังคับคดี) และค่าใช้จ่ายในการดำเนินงานที่ลดลง 4% (จากการรับรู้ผลขาดทุนจากการด้อยค่าของ NPA ที่น้อยลง)

อัตราผลตอบแทนจากเงินปันผลดี เราปรับประมาณการ DPS ปี 2569 ลดลงจาก 0.5 บาท เป็น 0.45 บาท (อัตราการจ่ายเงินปันผล 85%) เทียบกับ 0.5 บาท สำหรับปี 2568 (อัตราการจ่ายเงินปันผล 89%) ซึ่งยังคงให้อัตราตอบแทนที่ดีที่ 6.6%

คงคำแนะนำ OUTPERFORM แต่ปรับราคาเป้าหมายลดลง อัตราผลตอบแทนจากเงินปันผลที่ดีที่ 6.6% สำหรับปี 2569 และ upside จากโอกาสที่จะมีการจัดตั้ง JVAMC ใหม่ ทำให้เราคงคำแนะนำ OUTPERFORM สำหรับ BAM แต่ปรับราคาเป้าหมายลดลงจาก 8.5 บาท เป็น 7.5 บาท (อ้างอิงวิธี DDM) เพื่อสะท้อนการปรับลดประมาณการ DPS ปี 2569

ปัจจัยเสี่ยงที่สำคัญ: 1) ความเสี่ยงด้านการเรียกเก็บเงินสดจากภาวะเศรษฐกิจชะลอตัวและแรงกดดันเงินเฟ้อที่เพิ่มขึ้น 2) อุปสงค์ในตลาดอสังหาริมทรัพย์ชะลอตัวลง และ 3) การแข่งขันที่สูงขึ้นจากผู้เล่นรายใหม่

Preview 1Q26: Flat YoY, up QoQ; good div. yield

We forecast 1Q26F earnings to be flat YoY but up 84% QoQ, with weaker cash collection, easing credit cost and falling cost of funds. To factor in the rising inflationary pressure, we trim our 2026F by 3% and now expect a 5% decline. Though we cut TP to Bt7.5 from Bt8.5, we maintain OUTPEFFORM as dividend yield is still a good 6.6% and there is upside from potential new JVAMCs.

1Q26 preview: Flat YoY, up QoQ. We forecast 1Q26F earnings to be flattish YoY but surge 84% QoQ to Bt216mn, with: 1) expected cash collection of Bt3bn – down 6% YoY and 26% QoQ, 2) lower ECL due to lower reserve for the remaining cost of NPAs purchased from the Legal Execution Department and deterioration in asset quality, 3) a further 13 bps QoQ decline in cost of funds to 3.27%and 4) easing opex on smaller impairment losses on NPA.

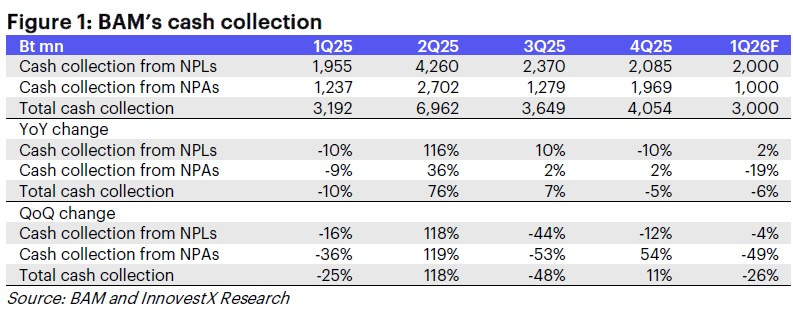

Cash collection: Down YoY and QoQ; cut 2026F. According to BAM’s IR officer, cash collection was ~Bt3bn in 1Q26, down 6% YoY and 26% QoQ, accounting for just 17% of its Bt17.9bn full-year target. As a result of rising inflationary pressure from the energy crisis arising from the Middle East conflict, we cut our 2026F cash collection assumption from Bt17.5bn to Bt16.5bn, representing an 8% decrease from 2025’s high base from two large-sized NPL and NPA deals.

Trim 2026F earnings. The 6% reduction in cash collection assumption trims 2026F earnings by 3%. We now expect 2026F earnings to fall 5% with an expected 8% fall in cash collection, a 20 bps fall in cost of funds, a 17 bps drop in credit cost (due to lower reserves for NPAs purchased from the Legal Execution Department) and a 4% decrease in opex (on smaller impairment losses on NPA).

Good dividend yield. We cut our 2026F DPS estimate from Bt0.5 to Bt0.45 (85% payout) vs. Bt0.5 for 2025 (89% payout), giving a still-solid yield of 6.6%.

Maintain OUTPERFORM with a TP cut. Dividend yield for 2026F is still good at 6.6% and with upside from the potential new JVAM, we maintain OUTPERFORM but cut TP to Bt7.5 (based on DDM) from Bt8.5 to reflect the lower 2026F DPS.

Key risks: 1) Cash collection risk from an economic slowdown and rising inflationary pressure, 2) a slowdown in property market demand and 3) rising competition from new players.

Download PDF Click > BAM260507_E.pdf